Concept 17: Law of Demand

Learn

Beginner

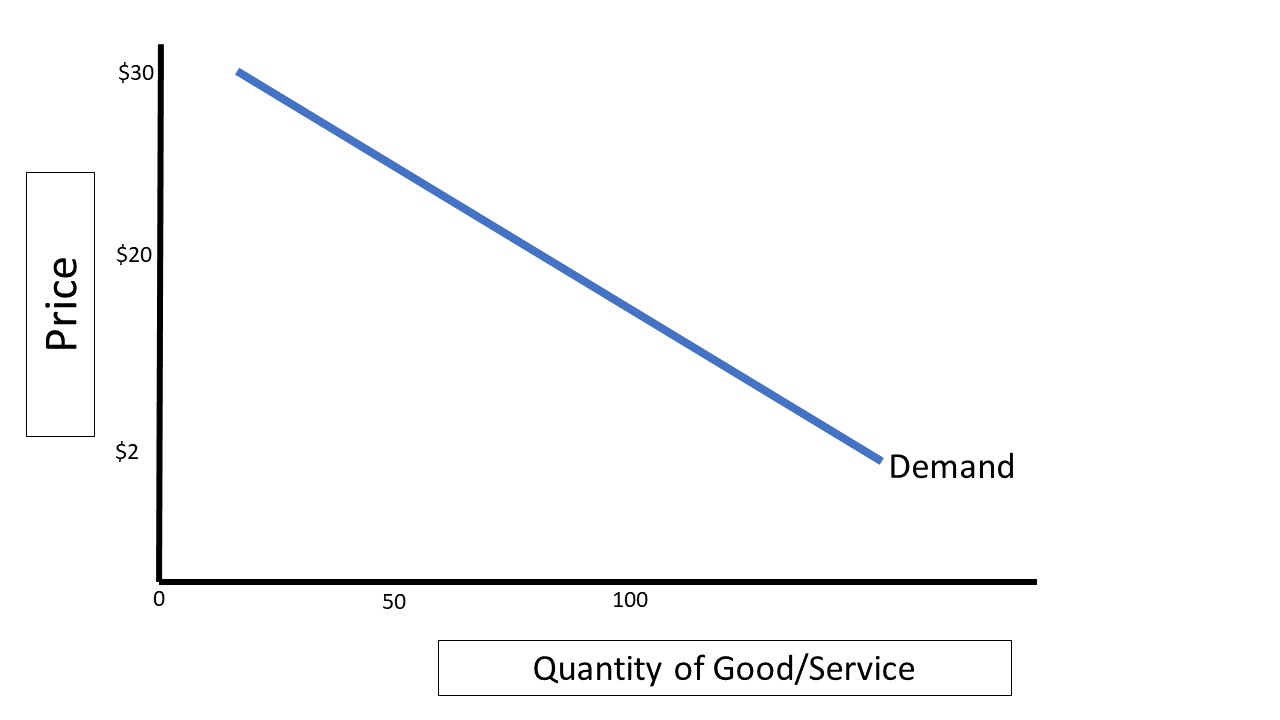

The Law of Demand states that there is an indirect relationship between the price of a good or service and the quantity of that good or service that consumers are willing and able to buy. In other words, as the price of an item increases, buyers are less willing and able to buy it and vice versa. The law of demand explains how consumers usually respond to price changes. Remember – quantity responds to price, not the other way around! A change in price leads to a decrease in quantity demanded only. Factors that change overall demand are dealt with in Concept 19 – Determinants of Demand. When graphed, the law of demand is shown by a downward sloping demand curve like the one seen in Graph 17-1.

Intermediate

Demand for a product requires willingness and ability to pay. Ability to pay is simple arithmetic. As the price of a good or service increases, a buyer’s ability to buy the same quantity decreases, even if the buyer still really wants it. If a cupcake costs $2 and you have $10, you can buy five cupcakes. If the price rises to $4 and you still have $10, you can only buy two.

Willingness to buy something is slightly more complicated. One aspect of your willingness to buy is how much satisfaction you think the good or service will bring you. As you consume more units of the same good (like cupcakes), your additional satisfaction with each new unit decreases, and you will be less willing to spend the same amount of money for it. Please see Concept 5: Marginal Cost and Marginal Benefit for further explanation.

Additionally, your willingness to buy something is affected by opportunity cost. In the cupcake example above, spending $2 on a cupcake is okay with many people because most $2 items give you about the same satisfaction. You’re not giving up anything too significant to get the cupcake. If the price of a cupcake becomes $10, however, there is potentially a much higher opportunity cost. You might be sacrificing an entire pizza for a single cupcake! You can spend $10 in more ways and on items that may bring more satisfaction, so your willingness to spend $10 on a single cupcake is lower. Thus, the quantity you demand is lower.

Advanced

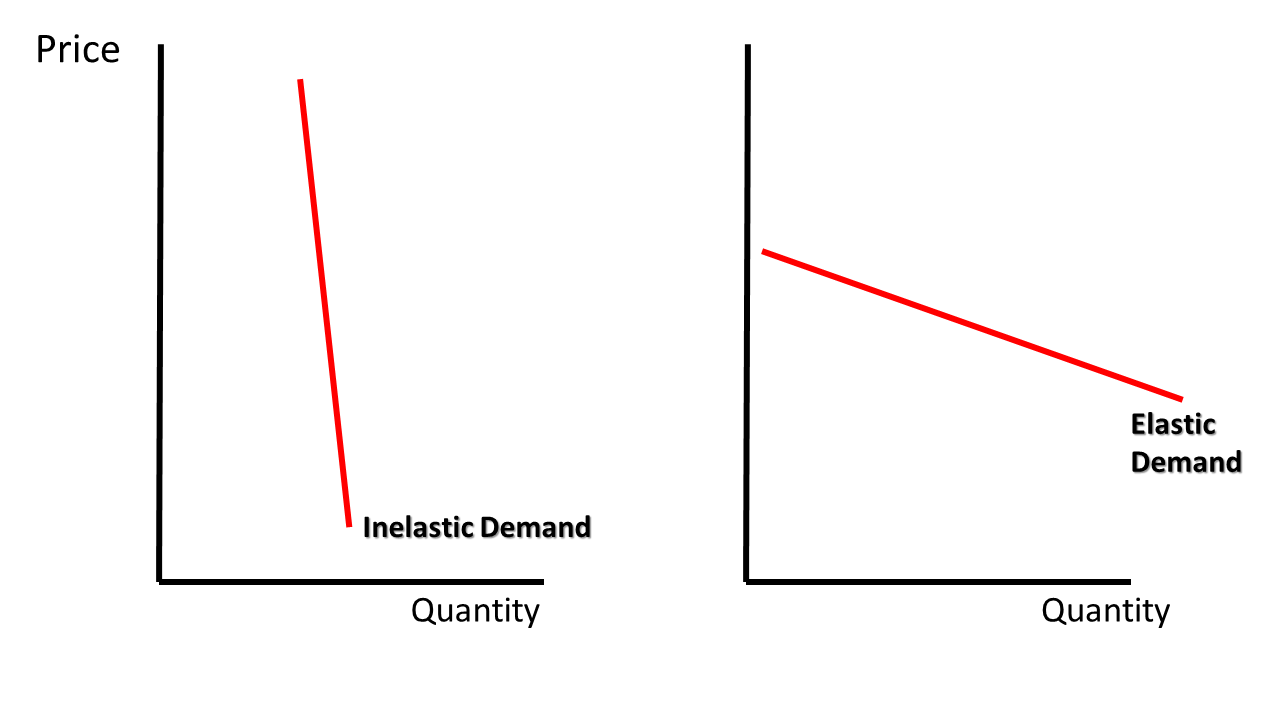

Like supply, demand can be elastic or inelastic. Elastic demand refers to a price or price range where a relatively small change in price leads to a relatively large change in quantity demanded. This is usually the case for products that have many substitutes or are not necessities. Inelastic demand refers to a situation where even with a large change in price, consumers purchase roughly the same quantity. Medicine, utilities, and – to some extent – gasoline are examples of this. Even when gas prices go up 15-20% people do not drive 15-20% less.

Click a reading level below or scroll down to practice this concept.

Practice

Assess

Below are five questions about this concept. Choose the one best answer for each question and be sure to read the feedback given. Click “next question” to move on when ready.

Social Studies 2024

Define the law of supply and the law of demand.