Concept 47: Use of Credit

Learn

Beginner

Credit refers to the ability of a person or business to make a purchase now and pay for it later. This is made possible through a lender, a person or an institution like a bank, that trusts they will be paid back later. Typically, the lender expects the borrower will repay the money they borrowed with interest. Interest is extra money that is paid by the borrower to the lender for the ability to use the loan money now. It’s the “price” of using money.

Credit (also known as debt) is commonly used for large purchases like houses, cars, college tuition, starting a business or emergencies like medical expenses. The borrower can make these large purchases and slowly repay them over time in smaller amounts. Other uses of credit include household daily purchases through credit cards, personal loans and business expenses like travel and even payroll. The availability of and access to credit has become a critically important cornerstone of the U.S. economy. About 60% of American homeowners, for example, have a mortgage loan that helped them buy their house.

Intermediate

Using credit has advantages and disadvantages. On the positive side, once you begin using credit you develop a credit history. As long as you make payments on time, your history will show that you are a responsible borrower and you will be able to borrow again in the future. Find out more about this in Concept 48 – Credit Worthiness. Another benefit is the ability to use money now that you won’t actually receive until the future. This allows people to make large purchases (like homes) that would otherwise require years or decades of saving. Responsible use of credit cards can also provide benefits like points for hotels or airlines and access to special events and deals.

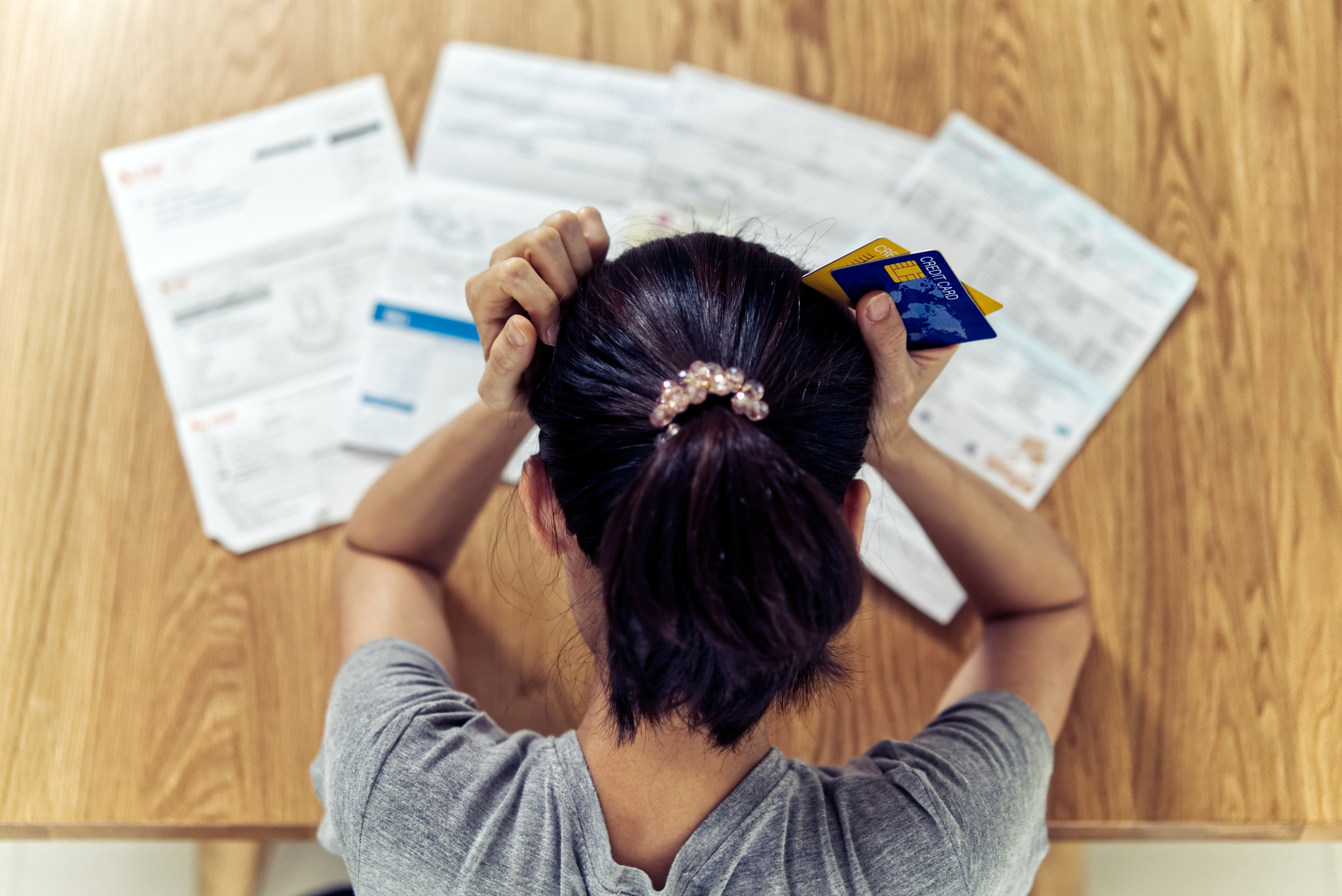

Even when used carefully, credit can make purchases more expensive. Something that costs $100 could end up costing $110 if purchased with a loan that carried a 10% interest rate. Mismanagement of credit can have profoundly serious consequences. Failing to repay money or make payments on time can ruin a person’s credit history, making it extremely difficult and expensive to access credit in the future. In some cases, people have to file bankruptcy and forego other assets or their wages to repay debt. Falling behind on payments can also cause interest rates on loans to increase, increasing the total amount owed.

Using credit is not to be taken lightly. Budgeting, paying more than the minimum required, understanding credit limits and the importance of repaying on time are all important skills to master before using credit.

Advanced

The previous section mentions many financial disadvantages to using credit. In the last decade or so more and more attention has been given to the mental and physical tolls debt can take as well. Studies from Northwestern University and the University of South Carolina have made strong links between student debt and depression, stress, self-reported unhappiness and even weight gain. In light of this and the credit crisis of 2008, many new laws and regulations have been put in place to control lenders and provide borrowers more information. Using credit should not be viewed as a good/bad scenario. Rather, borrowers need to make informed, rational decisions about credit and act in ways that benefit them.

Click a reading level below or scroll down to practice this concept.

Practice

Assess

Below are five questions about this concept. Choose the one best answer for each question and be sure to read the feedback given. Click “next question” to move on when ready.

Social Studies 2024

Evaluate the costs and benefits of using credit.